Few things strike fear in taxpayers like receiving an IRS audit notice. But while an audit can feel intimidating, understanding what triggers an IRS audit and how to respond effectively can put you back in control.

At Goldburd McCone LLP, we defend individuals and businesses facing audits every day — ensuring the IRS stays within its bounds and taxpayers’ rights are protected.

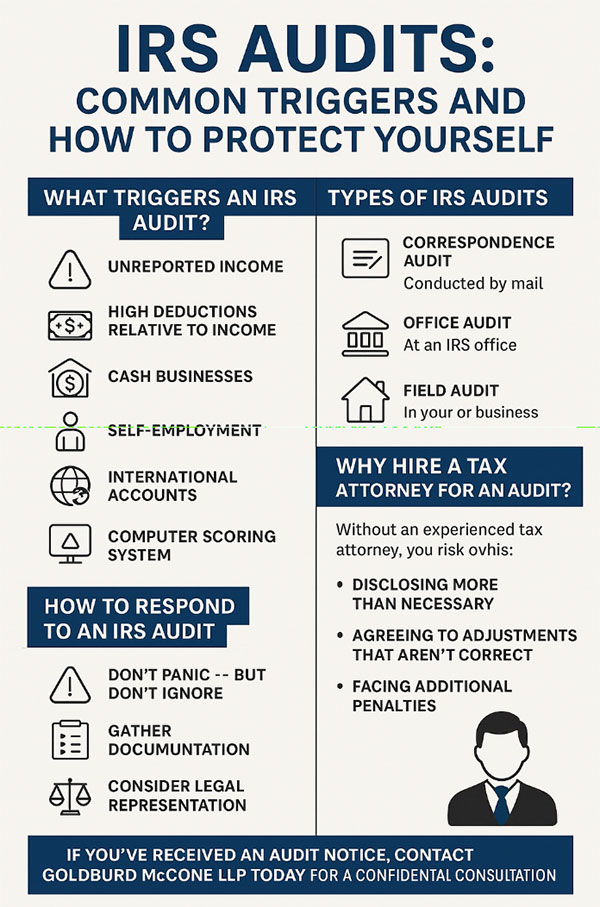

What Triggers an IRS Audit?

IRS audits aren’t random. While the IRS does conduct some random examinations, most audits are triggered by specific factors.

Unreported Income

You know all those forms you get in the mail each year—W-2s from your employer, 1099s from your bank, maybe a few from freelance clients?

Well, the IRS gets copies of every single one of these too.

When something doesn’t match up, even by a small amount, their system immediately takes notice.

It’s surprisingly easy to accidentally leave something off your return. Maybe you switched banks mid-year and forgot about that small interest payment from your old savings account. Or perhaps you did a one-off consulting gig and the 1099 got lost in your email.

Sometimes people genuinely forget about unemployment compensation they received early in the year.

Even a tiny discrepancy, say $50 in unreported interest, can trigger an inquiry.

That’s why keeping a folder (physical or digital) for all your tax documents throughout the year is so valuable. When tax time rolls around, you can cross-check everything against your records rather than relying on memory.

High Deductions Relative to Income

When your deductions are way outside the norms of your income, their systems take notice.

Now, this doesn’t mean you should be afraid to claim every legitimate deduction you’re entitled to—that’s your right as a taxpayer.

But if you donated half your income to charity last year, or if your home office deduction seems large relative to your income, you’ll want to make sure you’ve got rock-solid documentation.

We’re talking receipts, cancelled checks, acknowledgement letters from charities, etc.

The truth is, unusual situations do happen. Maybe you had extensive medical expenses due to an unexpected illness, or you made an exceptionally generous charitable contribution after selling some investments.

The IRS understands that real life doesn’t always fit neatly into statistical averages. But they’ll want to verify that these outlier deductions are real, so having your paperwork in order from the start saves everyone time and stress.

Cash Businesses

If you run a restaurant, hair salon, food truck, or any business where cash changes hands regularly, you’re probably already aware that the IRS pays closer attention to your industry.

It’s not that they think everyone in these businesses is dishonest—they just know from experience that cash creates opportunities for income to slip through the cracks, whether intentionally or through simple bookkeeping oversights.

Think about it from their perspective: when someone pays with a credit card, there’s an electronic trail. When they pay cash, the only record might be a handwritten receipt or a number jotted in a notebook.

That’s why businesses that deal heavily in cash need to be extra diligent about their record-keeping.

If this is you, consider making your life easier (and audit-proof) by depositing cash receipts regularly and keeping them intact—resist the temptation to take out your salary or pay expenses directly from the till.

Keep detailed daily records, maybe invest in a point-of-sale system that tracks everything automatically, and for heaven’s sake, keep your business and personal finances separate.

Yes, it’s more work, but it’s far less work than dealing with an audit. Plus, good records actually help you understand your business better, so it’s a win-win.

Self-Employment

Being self-employed comes with amazing freedom, but it also comes with increased IRS scrutiny.

Schedule C filers face audit rates several times higher than regular wage earners, and while that might seem unfair, there’s a certain logic to it.

When you’re self-employed, you have more control over how you report income and expenses, and the rules are genuinely more complex.

The IRS has seen it all when it comes to questionable Schedule C deductions—the person who claims their entire car payment as a business expense despite only using it for business 20% of the time, or the “consulting business” that reports losses year after year while the owner maintains a suspiciously comfortable lifestyle.

These patterns have made them skeptical, which means legitimate self-employed folks need to be extra careful.

If you’re self-employed, treat your business like a business, even if you’re working from your kitchen table.

Get a separate bank account and credit card for business expenses (this makes tax time so much easier anyway).

Keep a mileage log that would make your most detail-oriented friend proud. Save every receipt, and write notes on them about the business purpose if it’s not obvious.

And if your business has been losing money for several years, be prepared to show that you’re genuinely trying to make a profit—otherwise, the IRS might reclassify your business as a hobby, and there goes your ability to deduct those losses.

International Accounts

If you have money in foreign banks or investments overseas, you’re dealing with some of the most complex areas of tax law.

The IRS has really cracked down on international tax compliance over the past decade, and the penalties for getting it wrong can be absolutely crushing—we’re talking penalties that can exceed the value of the accounts themselves.

The tricky part is that the rules are genuinely confusing.

Many people don’t realize that their foreign mutual fund requires special reporting, or that the foreign bank account they inherited from their grandmother needs to be disclosed even if they never touch the money.

And if your foreign accounts total more than $10,000 at any point during the year, you need to file an FBAR. Miss that deadline, and you could face serious consequences.

If you have any international financial connections—whether it’s a bank account from when you worked abroad, foreign investments, or rental property in another country—don’t try to navigate this alone.

Find a tax professional who actually understands international taxation.

Computer Scoring System

The Discriminant Inventory Function (DIF) sounds like something out of a spy novel, but it’s actually the computer scoring system the IRS uses to decide which returns deserve a closer look.

Think of it as an incredibly sophisticated program that looks at hundreds of different factors on your return and compares them to millions of other returns to spot anything unusual.

Nobody outside the IRS knows exactly how the DIF formula works, it’s one of their most closely guarded secrets.

But we do know it looks at relationships between different numbers on your return. For instance, if you’re reporting a modest income but claiming mortgage interest on a million-dollar home, that’s going to raise questions. Or if your business expenses are completely out of line with others in your industry, the system will flag it.

The important thing to remember is that having a high DIF score doesn’t mean you’ve done anything wrong. Plenty of people have legitimate reasons for being statistical outliers.

Maybe you had an unusual financial event this year, or your situation is genuinely different from the norm. That’s fine—just make sure you can back up everything on your return with solid documentation.

The IRS knows that real life is messy and complicated. They just want to make sure that when someone’s return looks unusual, there’s a real story behind it, not creative accounting.

Types of IRS Audits

- Correspondence Audit – Conducted by mail; usually limited to specific issues.

- Office Audit – You are asked to appear at an IRS office with documents.

- Field Audit – IRS agents come to your home or business; the most intrusive type.

How to Respond to an IRS Audit

- Don’t panic — but don’t ignore. Respond promptly to deadlines.

- Gather documentation. Receipts, bank statements, invoices, contracts.

- Limit communication. Don’t overshare; only provide what is requested.

- Consider legal representation. A tax attorney ensures compliance while protecting you from unnecessary exposure.

- Appeal if necessary. If you disagree with audit findings, you have rights to reconsideration and appeals.

Why Hire a Tax Attorney for an Audit?

The IRS has skilled examiners whose job is to maximize tax collection. Without experienced representation, you risk:

- Disclosing more than necessary.

- Agreeing to adjustments that aren’t correct.

- Facing additional penalties.

Goldburd McCone LLP represents clients in New York, New Jersey, and nationwide to resolve audits efficiently and favorably.

Conclusion & CTA

An IRS audit doesn’t have to derail your finances. With the right strategy, you can respond effectively and protect your rights.

If you’ve received an audit notice, contact Goldburd McCone LLP today for a confidential consultation.