Goldburd McCone LLPGoldburd McCone LLP2026-07-15T13:00:32Zhttps://www.goldburdmccone.com/feed/atom/WordPress/wp-content/uploads/sites/1204345/2020/03/cropped-GM_SITEICON_512x512_MAR20-32x32.jpgOn Behalf of Goldburd McCone LLP<![CDATA[Surprising consequences of tax debt]]>https://www.goldburdmccone.com/?p=2608802026-06-11T10:40:45Z2026-06-23T10:39:56Z Internal Revenue Service (IRS) does not mess around when it comes to taxes. In addition to audits and investigations, those who fail to settle their tax bills can find themselves facing surprising repercussions. Three examples include the loss of refunds, loss of funds directly from paychecks and limited ability to leave the country.

#1: Recapture refunds

There are instances when the IRS can recapture, or essentially keep, a taxpayer’s tax refund. The IRS can recapture or offset the tax refund for past due federal taxes until the taxpayer settles the debt.

#2: Levy

Depending on the details of the tax debt, the IRS can pursue a levy. A levy is a legal tool that allows the agency to directly garnish wages from the taxpayer’s bank or other accounts. It can also allow the government to seize property like vehicles or real estate. This action is generally preceded by a Final Notice of Intent to Levy and Notice of Your Right to a Hearing. Anyone who receives these documents is wise to take the matter seriously and consider alternative options to deal with their tax bill.

#3: Passport denials

The IRS can also limit the ability for taxpayers to leave the country when seriously delinquent with their tax obligations. This involves collaboration with the State Department who would deny the taxpayer’s application for a passport or revoke a currently held passport. In 2026, the IRS considers a taxpayer’s obligations “seriously delinquent” when at or above $66,000.

Options to manage tax debt

Those who find themselves facing an unmanageable tax bill have options, including the IRS Fresh Start Initiative. The agency has stated the program is focused on helping taxpayers get back on track. The reality is taxpayers who are considering pursuing these options should tread carefully as qualifying for the offerings included in the initiative is not an easy process. Offerings include penalty relief, offers in compromise and repayment plans. The repayment plans can be short or long-term. The short term plan generally extends payments over a period of 180 days while the long-term plan, also known as installment agreements, provides additional time. The application process can be complex and denials are common. Tax debt can create problems that go beyond a tax bill. In addition to penalty fees and fines, taxpayers can find themselves dealing with lost refunds, wages and property as well as difficulties with travel. Legal counsel with experience in this niche area of law can help review options and help you to find a path forward.]]>On Behalf of Goldburd McCone LLP<![CDATA[Why repayment stress is rising for SBA borrowers]]>https://www.goldburdmccone.com/?p=2608252026-04-02T13:02:32Z2026-04-14T20:12:55Z payments are coming due; interest rates are higher than they were a few years ago and many small business owners are discovering that “affordable” SBA financing can feel far less manageable in today’s environment. For a growing number of SBA borrowers, repayment stress is not just a passing worry — it is becoming a persistent pressure that affects cash flow decisions, hiring plans and day-to-day operations.

In this post, we will explore why repayment stress is rising for SBA borrowers, what is driving the shift and options for business owners that are struggling to make ends meet.

Why is repayment stress on the rise?

Many small business owners took Small Business Administration (SBA) loans to stabilize operations during volatile conditions. A prime example being the pandemic. Repayment now collides with higher costs, elevated interest rates and delayed receivables. In legal terms, repayment distress creates immediate issues for borrowers potentially including defaults for missed payments. This can compound the issue, adding frustration to an already difficult situation.Borrowers who find themselves in this situation are not alone. According to a recent report in The New York Times, the SBA has referred over $75 billion in delinquent loans to the Treasury Department for collection. Business owners should note that they are in the crosshairs of experienced federal collection officers. The Treasury Department’s Bureau of Fiscal Services is aggressive about these collection efforts. They may refer delinquent loans to credit reporting services and garnish funds directly from tax refunds and Social Security payments. Those who used assets to personally guarantee the loan can find themselves facing liens on their homes and businesses.

What options are available for business owners struggling to meet repayment demands?

There is the possibility that lawmakers will step in and offer additional relief. Legal counsel with experience in this area has voiced concern and expect the Treasury or Congress to step in. The piece in The New York Times quoted Benjamin Goldburd, an attorney with experience in tax and corporate matters who has seen a “deluge” of small business owners in this predicament, stated such intervention seems likely as the government does not want to pursue hundreds of thousands of lawsuits against small business owners. In the meantime, small business owners are wise to seek legal counsel with experience in this niche area of law to review the particulars of their case and help determine the best course of action. Options could include payment assistance, forgiveness, discharge and offers in compromise. ]]>On Behalf of Goldburd McCone LLP<![CDATA[What is the role of AI in tax audits?]]>https://www.goldburdmccone.com/?p=2607182026-02-10T14:51:55Z2026-02-10T14:51:55Z family photos repurposed to reflect various occasions on social media to virtual assistants offering help whenever we call and make an appointment to see a doctor, artificial intelligence (AI) is taking the world by storm. Even the government is making use of this tool. We know that the Internal Revenue Service (IRS) is using AI tools to help increase efficiency of tax reviews – but it may come as a surprise that state taxing authorities may be even more aggressive in their use of this new tool.

State taxing authorities are using AI to find taxpayers who are failing to pay their income tax obligations. This is especially true in high income tax states like New York where the state taxing authority states it conducted over 770,000 audits in 2022 alone. This is a 56% increase from the previous year.

How are state taxing authorities using AI?

State taxing authorities can use AI to review massive amounts of data to root out taxpayers who may require a closer look. Recent reports show that the New York Department of Taxation and Finance has sent a large number of inquiry letters to taxpayers. These letters are focused on questions about residency changes and remote work status.

What is the New York Department of Taxation and Finance looking for?

When it comes down to it, they want your money. They want to establish that even though you claim to live in a different state, you still owe New York taxes. An investigation by state taxing authorities will dig into every area of your life to try to find evidence that you still consider New York home. This could include looking into whether you still own property in the state, what type of items you keep in the state, and even the location of the veterinarian you use for your family pet. Even if you clearly live in another state, they will argue you still owe taxes if your company is a New York company with a New York office. Critics argue that the reliance on AI has led to too many inquiry letters without enough evidence to support an audit. This means innocent taxpayers could find themselves in the agency’s crosshairs.

What should I do if I get an inquiry letter?

The first step is to take the letter seriously. Review it carefully for any important deadlines and to get a better idea of the supposed issue. Next, reach out to legal counsel with experience in this area of law. The tax laws that guide these claims are complex and ever evolving, making experienced counsel an important step towards mitigating the impact of the allegations. Even those who do not receive an inquiry letter are wise to take these developments as a reminder to review their tax saving strategies for compliance. Careful review can help address any concerns before they grow into a bigger problem.]]>On Behalf of Goldburd McCone LLP<![CDATA[What are the Four Types of Innocent Spouse Relief?]]>https://www.goldburdmccone.com/?p=2606542026-01-07T21:47:09Z2026-01-07T21:45:35ZThe IRS recognizes that holding innocent spouses responsible for their partner's tax misdeeds can be fundamentally unjust. Through a set of provisions collectively known as "Innocent Spouse Relief," you may be able to escape liability for tax debts you didn't create or know about. These programs can release you from paying taxes, interest, and penalties that rightfully belong to your current or former spouse.

What is Innocent Spouse Relief?

Innocent Spouse Relief encompasses a collection of IRS provisions designed to protect individuals from being held responsible for tax debts arising from their spouse's or ex-spouse's improper actions on a joint tax return. These programs recognize that marriage shouldn't mean accepting unlimited financial liability for a partner's deceptions, mistakes, or financial irresponsibility.The relief separates your tax liability from your spouse's, creating individual responsibility where the IRS previously saw only joint obligation.

The 4 Types of Spousal Tax Relief Explained

The IRS offers four distinct forms of spousal tax relief, each designed for different situations and providing different types of protection. Three of these—Classic Innocent Spouse Relief, Separation of Liability Relief, and Equitable Relief—are requested using Form 8857 and deal with errors or unpaid taxes on joint returns. The fourth, Injured Spouse Relief, uses Form 8379 and protects your share of a tax refund from being seized for your spouse's separate debts. Understanding which type fits your situation is crucial for successful relief.

1. "Classic" Innocent Spouse Relief

Classic Innocent Spouse Relief provides complete freedom from tax liability when your spouse or ex-spouse committed tax fraud or errors that you knew nothing about. This is the gold standard of relief—if granted, you pay nothing toward the understated tax, no matter how large the debt.This relief applies when your spouse failed to report income, claimed bogus deductions, or manipulated the return in ways that reduced the tax owed. Maybe they had a side business you knew nothing about, received cash payments they never mentioned, or fabricated charitable donations. The key is that these errors created an "understated tax"—the return showed less tax than was actually owed.Who Qualifies? (Eligibility Checklist):

You filed a joint return that has an understated tax due to erroneous items attributable to your spouse

When you signed the return, you didn't know and had no reason to know about the understated tax

After examining all facts and circumstances, the IRS determines it would be unfair to hold you liable

You and your spouse aren't engaged in transferring assets as part of a fraudulent scheme

Best for: Situations involving hidden income, secret businesses, fraudulent deductions, or any tax understatement you were genuinely unaware of when signing the return.

2. Separation of Liability Relief

Separation of Liability Relief divides the tax debt between you and your spouse based on each person's actual contribution to the tax understatement. Instead of being liable for 100% of the debt, you become responsible only for the portion attributable to your own income and deductions. If your spouse failed to report $50,000 in business income while you accurately reported your $30,000 salary, you'd only be responsible for taxes on your earnings.This relief doesn't provide refunds for taxes already paid—it only affects remaining unpaid balances. The IRS essentially recreates what your individual tax liability would have been if you'd filed separate returns, then limits your responsibility to that amount.Who Qualifies? (Eligibility Checklist):

You filed a joint return with an understated tax

You're now divorced or legally separated from the spouse with whom you filed the joint return, OR

You haven't lived in the same household as that spouse for the 12 months before filing for relief

You didn't have actual knowledge of the erroneous items when you signed the return

Best for: Divorced or separated individuals who want to limit their liability to their fair share of the tax debt, particularly when they can clearly demonstrate which spouse's actions caused the understatement.

3. Equitable Relief

Equitable Relief serves as the safety net for those who don't qualify for the other types but face circumstances that make holding them liable fundamentally unfair. This is the most flexible and subjective form of relief, allowing the IRS to consider the totality of your situation rather than applying rigid criteria.Unlike the other forms, Equitable Relief applies to both understated taxes (errors on the return) and underpayments (correctly reported taxes that were never paid). It's designed for complex situations where strict rule application would create injustice—cases involving domestic abuse, financial control, severe economic hardship, or reasonable reliance on a spouse's promise to pay.Who Qualifies? (Factors the IRS Considers):

You don't qualify for Classic Innocent Spouse or Separation of Liability Relief

Economic hardship would result if relief isn't granted (you'd be unable to pay basic living expenses)

You suffered abuse or were subject to financial control by your spouse

You didn't know or have reason to know about the error, or reasonably expected your spouse to pay

You didn't significantly benefit beyond normal support from the unpaid taxes

Mental or physical health issues affected your involvement in tax matters

The tax liability is solely attributable to your spouse's actions

Best for: Cases involving domestic abuse, financial control, economic hardship, or situations where you knew about the tax but had reasonable grounds to believe your spouse would pay it.

4. Injured Spouse Relief (A Different Kind of Relief)

Injured Spouse Relief stands apart from the other three types—it has nothing to do with errors on your tax return or unpaid taxes. Instead, this relief protects your portion of a tax refund when the IRS seizes it to pay your spouse's separate debts from before your marriage or unrelated to your joint finances.Imagine filing a joint return expecting a $5,000 refund from your tax withholdings, only to receive nothing because the IRS applied the entire amount to your spouse's defaulted student loans from before you met. Injured Spouse Relief allows you to reclaim your share of that refund—the portion attributable to your income and tax payments.Who Qualifies? (Eligibility Checklist):

You filed a joint return and are due a refund

Your spouse has a past-due federal or state debt (child support, student loans, prior tax debt)

You're not legally obligated for the debt (it preceded your marriage or arose from your spouse's separate obligation)

You reported income or made tax payments on the joint return

Best for: Protecting your share of a current tax refund from being seized for your spouse's pre-existing debts like child support, defaulted student loans, or old tax obligations.

Critical Deadlines to File

Missing these deadlines can permanently bar you from relief, regardless of how strong your case might be:Form 8857 (Innocent Spouse, Separation of Liability, Equitable Relief): You must file within 2 years from the date the IRS first attempted to collect the tax from you. This isn't when the tax was assessed—it's when they sent the first collection notice to you personally or took collection action like garnishing wages.Form 8379 (Injured Spouse): You have 3 years from the original return's due date or 2 years from when you paid the tax, whichever is later. For the most recent tax year, you can file it with your return.

Get Expert Help with Your Innocent Spouse Relief Case

Navigating the innocent spouse relief process while dealing with the emotional and financial stress of unexpected tax debt can feel overwhelming. At Goldburd McCone LLP, our experienced tax attorneys have successfully guided countless clients through innocent spouse relief applications, helping them escape unfair tax burdens and protect their financial futures. We understand the nuances of each relief type, know what documentation strengthens your case, and can craft compelling arguments that resonate with IRS decision-makers.

Frequently Asked Questions

What's the main difference between Innocent Spouse and Injured Spouse Relief?

Innocent Spouse Relief frees you from paying tax debts caused by errors or fraud on a joint return—you're seeking relief from a tax liability. Injured Spouse Relief protects your share of a tax refund from being seized for your spouse's separate pre-existing debts—you're protecting money you're already owed. They address completely different problems despite the similar names.

Will my ex-spouse be notified if I apply? What about my privacy?

Yes, federal law requires the IRS to notify your spouse or ex-spouse about your innocent spouse request and give them an opportunity to participate in the process. However, the IRS will protect your privacy—they won't share your current address, phone number, employer, or other personal information with your ex. You can also redact sensitive information from supporting documents before submitting them.

What happens if the IRS denies my request?

If the IRS issues an unfavorable preliminary determination, you have 30 days to appeal to the IRS Office of Appeals, where an independent officer will review your case. If Appeals upholds the denial, you can petition the U.S. Tax Court within 90 days of the final determination. The Tax Court provides an independent judicial review and has sometimes overruled IRS denials, particularly in equitable relief cases.]]>On Behalf of Goldburd McCone LLP<![CDATA[How to Handle IRS Tax Collection Issues: Liens, Levies, and Repayment Plans]]>https://www.goldburdmccone.com/?p=2606522026-01-07T23:16:47Z2026-01-07T21:31:22ZDealing with the IRS can be overwhelming—especially when they are making collection moves like placing liens or levying bank accounts. If you’re facing delinquent tax debt, know this: you do have options.

What is an IRS Lien?

An IRS lien is essentially the government planting a flag on everything you own, saying "we have a legal claim to this until you pay your tax debt." It's important to understand that a lien doesn't mean they're taking your property right now—think of it more like a mortgage company having an interest in your house. The property is still yours to use, but the IRS has secured their interest in it.

What is an IRS Levy?

Unlike a lien, which is more of a legal technicality that complicates your financial life, a levy involves the IRS actually seizing your assets to satisfy your tax debt.The most common type of levy is a bank levy. Here's how it typically plays out: You wake up one morning, check your bank account to make sure your direct deposit hit, and find your balance is zero.Or worse, you're at the grocery store, your card gets declined, and you discover the IRS has frozen your account. When the IRS levies your bank account, the bank is required to hold the funds for 21 days before sending them to the IRS. This 21-day window is your last chance to resolve the issue before the money is gone for good.

Other Tools: The IRS's Expanding Collection Powers

Beyond liens and levies, the IRS has been granted additional collection tools over the years that can impact your daily life in ways you might not expect. These newer enforcement mechanisms show just how serious the government is about collecting tax debts.Passport Revocation is one of the more dramatic tools in the IRS's arsenal. If you owe more than $62,000 in tax debt (this threshold adjusts annually for inflation), the IRS can certify your debt to the State Department, which can then revoke your existing passport or refuse to issue or renew one. Imagine planning an international business trip or family vacation, only to find out at the airport that your passport has been revoked. For people who travel internationally for work, this can be career-ending. The only way to get your passport back is to pay the debt in full, set up an installment agreement, or otherwise resolve your tax situation.Driver's License Suspension isn't directly done by the IRS, but many states have programs where they'll suspend your driver's license if you have significant unpaid state taxes. Some states are also starting to share information with the IRS about federal tax debts. Losing your ability to drive legally can make it impossible to get to work, which creates a vicious cycle—you need to work to pay your tax debt, but you can't get to work without a license.Trust Fund Recovery Penalty (TFRP) assessments are particularly nasty surprises for business owners and anyone considered a "responsible person" in a business. If a business fails to pay its payroll taxes (the taxes withheld from employees' paychecks), the IRS can assess the Trust Fund Recovery Penalty against individuals personally. This means if you're a business owner, CFO, or even sometimes a bookkeeper with check-signing authority, you could be held personally liable for the business's unpaid payroll taxes. Professional License Suspension is another tool some states use, where they'll suspend professional licenses (medical, legal, contractor, real estate, etc.) for unpaid taxes. While this is typically a state-level action for state taxes, some states are beginning to coordinate with federal tax authorities.Seizure of Government Payments and Benefits extends beyond just Social Security. The IRS can intercept federal vendor payments if you do business with the government, federal employee retirement benefits, and even some federal grants. During tax season, they automatically grab any federal tax refunds you might be owed and apply them to your old debt—a process called a refund offset.Public Shaming and Business Consequences might not be official IRS tools, but they're real consequences of collection actions. In some jurisdictions, lists of delinquent taxpayers are published online. Business credit reports often show tax liens and levies, making it difficult to get trade credit or favorable payment terms from suppliers. Some professional organizations and licensing boards consider tax problems when evaluating members or renewal applications.The IRS does typically offer payment plans, hardship programs, and other alternatives that can help you avoid these harsh collection actions.These actions are serious. They can damage credit, cost you money in fees, and in worst cases, take property you value. The IRS doesn’t always get it right, which is why it’s worth reviewing the accuracy of what's owed.

Key Options to Resolve Collection Issues

Finding yourself on the wrong side of IRS collections can feel overwhelming, but here's something that might surprise you: the IRS actually wants to work with you. They'd much rather have a cooperative taxpayer making payments than spend resources on aggressive collection actions. That's why they've created multiple programs and options to help people resolve their tax debts. The trick is knowing which option fits your situation and how to navigate the application process successfully.Let's explore each of these resolution options in detail, so you can understand not just what they are, but when they make sense, how to qualify, and what to expect if you pursue them.

Installment Agreements

An installment agreement is essentially a payment plan with the IRS, and it's by far the most common way people resolve tax debts. Think of it like financing a car, except instead of driving off the lot with a new vehicle, you're buying yourself peace of mind and protection from aggressive collection actions. For many taxpayers, this is the sweet spot between what they owe and what they can realistically afford to pay.The beauty of an installment agreement is its simplicity and accessibility. If you owe less than $50,000 and can pay off the balance within 72 months, you can often set up a streamlined agreement online without even talking to anyone or providing financial documentation.

Offer in Compromise

An Offer in Compromise (OIC) is what everyone hopes for—the chance to settle your tax debt for less than the full amount owed. It's the IRS saying, "Okay, we'll take what we can get rather than nothing at all." But despite what those late-night TV commercials suggest, getting an OIC approved isn't easy, and it's definitely not available to everyone.The IRS accepts offers in compromise for three reasons: doubt as to collectibility (you genuinely can't pay the full amount), doubt as to liability (there's a legitimate dispute about whether you actually owe the tax), or effective tax administration (paying the full amount would create an economic hardship or would be unfair and inequitable).

Penalty Abatement

Penalties and interest can easily double or triple your original tax debt if left unchecked. The good news is that unlike the underlying tax, penalties can sometimes be reduced or eliminated entirely through penalty abatement.One strategic consideration: if you qualify for first-time abatement, think carefully about when to use it. Since you can only use it once every three years, you might want to save it for the tax period with the highest penalties. Also, if you're negotiating an offer in compromise or installment agreement, you might want to wait until after that's settled to request abatement, as the reduced balance could affect your negotiations.

Innocent Spouse Relief

The IRS doesn't think you should be held responsible for your spouse's tax crimes or omissions that you knew nothing about. Innocent spouse relief can release you from joint liability for taxes, penalties, and interest that should be solely your spouse's responsibility. It's a recognition that sometimes one spouse controls the finances, hides income, or claims fraudulent deductions without the other's knowledge.There are actually three types of relief available: innocent spouse relief, separation of liability, and equitable relief. Classic innocent spouse relief applies when your spouse (or ex-spouse) improperly reported or omitted items on your joint return without your knowledge. Separation of liability allows you to allocate tax liability between you and your former spouse. Equitable relief is the catch-all for situations that don't fit the other categories but where it would be unfair to hold you liable.The requirements for innocent spouse relief are strict. You must have filed a joint return with an understatement of tax due to erroneous items attributable to your spouse. You must establish that you didn't know and had no reason to know about the understatement. And it must be unfair to hold you liable considering all facts and circumstances.Timing is critical for innocent spouse relief. Generally, you must request relief within two years after the IRS first attempts to collect the tax from you. However, equitable relief has a longer timeline—you can request it within the period the IRS can collect the tax (generally 10 years from assessment) or within two years after payment if you're seeking refund of taxes paid.

Discharge Through Bankruptcy

For income tax debt to be dischargeable in Chapter 7 bankruptcy, it must meet five criteria:

the tax debt must be at least three years old (from the due date of the return)

the return must have been filed at least two years ago

the tax must have been assessed at least 240 days ago

the return must not be fraudulent

you must not have committed tax evasion.

Chapter 13 bankruptcy offers different advantages for tax debt. While it doesn't eliminate tax debt as readily as Chapter 7, it can provide a structured 3-5 year payment plan that might be more favorable than what the IRS would offer directly. Priority tax debts (recent income taxes, employment taxes) must be paid in full through the plan, but without additional penalties and sometimes with reduced interest. Non-priority tax debts might be paid at pennies on the dollar or discharged entirely.What makes bankruptcy complicated for tax debts is the classification system. Tax debts are categorized as secured (if there's a filed tax lien), priority unsecured (recent taxes, trust fund taxes), or general unsecured (older taxes meeting discharge criteria).One strategic consideration often overlooked: the timing of bankruptcy filing can dramatically affect which tax debts are dischargeable. Filing a few months too early might mean a significant tax debt doesn't meet the age requirements. Conversely, waiting too long might allow the IRS to file a lien, converting unsecured debt to secured debt that must be addressed differently in bankruptcy.

Release of Liens & Levies

Once you've resolved your tax debt or made arrangements with the IRS, getting liens and levies released should be a priority.For levies, release can happen relatively quickly once you've addressed the underlying issue. If you've set up an installment agreement, proven financial hardship, or paid the debt, the IRS will typically release a levy within days. Wage levies stop with the next payroll cycle after release. Bank levies are released before the 21-day holding period expires if you act quickly.Liens are more complicated. By law, the IRS must release a lien within 30 days after the tax debt is fully satisfied. But "release" doesn't mean the lien disappears from public records—it just shows as released. For many taxpayers, particularly those trying to rebuild credit or refinance property, a lien withdrawal is preferable. This actually removes the lien from public records as if it never existed.Understanding these resolution options is empowering, but choosing the right one—or combination—requires careful analysis of your specific situation.

Why Legal Representation Helps

Here’s why having an experienced advocate can be one of the best investments you make during a tax crisis.

Accuracy

A skilled tax lawyer knows how to scrutinize every line of an IRS assessment with a detective's eye. They understand the complex interplay between different sections of the tax code and can spot when the IRS has misapplied the law to your situation.

Experience with Negotiation

The IRS operates according to strict procedures, formulas, and guidelines that aren't always intuitive or publicly well-documented. Knowing these internal procedures—and more importantly, knowing how to work within them to your advantage—can make an enormous difference in the outcome.

Avoiding Worst Outcomes

One of the most valuable things a tax lawyer brings is the ability to prevent bad situations from becoming catastrophic. They understand the IRS collection process and know exactly what triggers escalation from one enforcement level to the next. More importantly, they know how to intervene at critical moments to prevent irreversible consequences.

Protecting Rights

A tax attorney serves as your advocate, ensuring the IRS follows proper procedures and respects your rights throughout the collection process. They know when the IRS is overstepping its bounds and how to push back effectively.

What To Do If You're Facing Collection Action

When facing IRS collection actions, every day matters. The IRS follows a predictable escalation pattern—from notices to liens to levies to asset seizure—and each step becomes progressively harder and more expensive to reverse. The key to a favorable resolution is taking swift, strategic action before your options narrow and enforcement actions become irreversible.The most critical steps you can take right now are simple but essential: Don't ignore IRS notices—each one contains important deadlines and rights that expire if you miss them. Gather all relevant documents including tax returns, financial records, and any correspondence with the IRS. Most importantly, understand that you have options beyond just paying in full—from installment agreements and Offers in Compromise to penalty abatement and Currently Not Collectible status. The right strategy depends entirely on your specific situation, and navigating these options while avoiding costly mistakes requires deep knowledge of IRS procedures and negotiation tactics.

Let Goldburd McCone Protect Your Rights and Resolve Your Tax Crisis

At Goldburd McCone, we've spent decades helping taxpayers escape the nightmare of IRS collections. Our experienced tax attorneys know how to stop aggressive collection actions, identify errors in IRS assessments, and negotiate the best possible resolution for your unique situation. We've successfully reduced tax debts by hundreds of thousands of dollars, removed penalties, released liens and levies, and helped countless clients get their lives back on track.]]>On Behalf of Goldburd McCone LLP<![CDATA[IRS Audit Reconsideration Explained]]>https://www.goldburdmccone.com/?p=2606502026-01-07T23:13:56Z2026-01-07T21:16:15ZWhat happens if the IRS audits you, makes adjustments, and you don’t agree with the results? Fortunately, there’s a process called audit reconsideration — your chance to correct errors or provide new evidence. At Goldburd McCone LLP, we regularly help clients pursue audit reconsideration to reduce or eliminate unfair tax liabilities.

What Is Audit Reconsideration?

Audit reconsideration is an IRS procedure that allows taxpayers to challenge a tax assessment after an audit has closed. Unlike an appeal, it’s not a formal court case, but rather an administrative review.

When Can You Request Audit Reconsideration?

The IRS doesn't grant reconsiderations just because you're unhappy with an audit outcome—there need to be specific, valid reasons why the original assessment might be incorrect. Knowing these qualifying scenarios is crucial because requesting reconsideration without proper grounds wastes both your time and the IRS's resources.

You Did Not Appear for Your Audit: When Life Gets in the Way

Sometimes life throws us curveballs at the worst possible moments. Maybe you were dealing with a medical emergency when the audit notice arrived, or perhaps you were deployed overseas with the military. When you don't show up for an audit, the IRS doesn't just forget about it. They proceed without you, making determinations based solely on the information they have—which usually isn't in your favor.

You Have New Documentation the IRS Didn't Review: Finding the Missing Pieces

This is probably the most common reason for requesting reconsideration, and it makes perfect sense when you think about it. Sometimes during an audit, you simply can't locate all the documentation you need. Maybe your ex-spouse had the receipts in question, or perhaps they were in a storage unit you couldn't access.New documentation can take many forms. It might be receipts you finally tracked down from a contractor who went out of business, bank statements from an account you'd forgotten about that prove your business expenses, or medical records that substantiate your claimed medical deductions.But here's the important part: "new" documentation doesn't mean "newly created" documentation. The IRS is looking for contemporaneous records—documents that existed at the time of the transaction or deduction in question. The key to success with new documentation is explaining clearly why this information wasn't available during the original audit and demonstrating how it directly addresses the IRS's concerns.

You Believe the IRS Made a Computational or Processing Error

It might surprise you to learn that yes, the IRS does make mistakes. They're human beings working with complex tax laws and massive amounts of data, and errors happen more often than you might think.Computational errors are the most straightforward—maybe they added up your income incorrectly, applied the wrong tax rate, or made a simple arithmetic mistake when calculating penalties and interest.Processing errors are a bit more complex and might involve the IRS misunderstanding your filing status, applying the wrong year's tax rates, or not giving you credit for payments you've already made.More subtle errors might involve the IRS misinterpreting the facts of your case. Perhaps they classified your legitimate business as a hobby, treated capital gains as ordinary income, or didn't recognize that certain expenses were ordinary and necessary for your type of business.When requesting reconsideration based on IRS error, specificity is your friend. Don't just say "you made a mistake"—identify exactly what the error was, show your calculations or reasoning, and provide any relevant tax law citations or IRS publications that support your position. If you can make it easy for them to see and correct their errors, you're much more likely to get a favorable outcome.

The Tax Assessed Is Still Unpaid

This requirement might seem counterintuitive at first. Why does it matter whether you've paid the tax if you're arguing you don't owe it? The answer lies in the different procedures the IRS has for handling disputes, and understanding this can save you from choosing the wrong path for your situation.If you've already paid the tax from the audit, your remedy isn't audit reconsideration—it's filing a claim for refund. These are two different processes with different requirements and timelines. Audit reconsideration is specifically for adjusting assessments that haven't been fully paid. Once you've paid, you're essentially saying "I paid this, but I want it back," which triggers the refund claim process instead.This distinction is particularly important if you're approaching statute of limitations deadlines. Claims for refund have specific time limits (generally two years from when you paid the tax or three years from when the return was filed, whichever is later), while audit reconsideration requests can sometimes be made even after these deadlines have passed, as long as the tax remains unpaid and collectible.Now, "unpaid" doesn't necessarily mean you haven't made any payments at all. If you've been making installment payments but haven't paid the full amount, or if the IRS has been collecting through wage garnishments but the debt isn't satisfied, you can still request reconsideration for the unpaid portion. The key is that there's still an outstanding balance that could be reduced or eliminated if the reconsideration is successful.

The Audit Reconsideration Process

Once you've determined that you qualify for audit reconsideration, the next challenge is navigating the actual process.

Form 12661

Form 12661, "Disputed Issue Verification," might not have the most exciting name, but it's your ticket to getting the IRS to reconsider your case. This form is actually more straightforward than many IRS documents, but that doesn't mean you should rush through it. Think of it as your opening statement in a legal case—it sets the tone for everything that follows.

Provide Supporting Evidence

This is where your case lives or dies. The IRS operates on documentation, not promises or explanations. Every claim you make needs to be backed up with paper (or digital) proof. But here's the thing—it's not just about quantity. Dumping a shoebox full of receipts on the IRS without organization or explanation is almost as bad as having no documentation at all.

Wait for IRS Review

Now comes perhaps the hardest part of the entire process: waiting. The IRS doesn't work on your timeline, and audit reconsiderations aren't considered urgent matters in their workflow. While they don't publish official timeframes for reconsideration reviews, it typically takes anywhere from three to six months, and complex cases can take even longer.During this waiting period, you might not hear anything at all from the IRS. This silence doesn't mean they've forgotten about you—it's just how the process works.While you're waiting, continue to monitor your mail carefully. If the IRS needs additional information, they'll send a letter with a specific deadline for response.

Possible Outcomes

When the IRS finally completes their review, you'll receive a letter explaining their determination. Understanding the possible outcomes can help you prepare for what comes next and decide whether further action is necessary.Reduction of Tax Owed is often the most realistic best-case scenario. The IRS might agree with some of your arguments but not others, resulting in a partial win.For example, they might accept your documentation for business expenses but maintain their position on your home office deduction.Elimination of Tax Liability is what everyone hopes for but few achieve. This happens when the IRS agrees completely with your position and determines that the original audit assessment was entirely incorrect. You might see this in cases where the IRS made a clear error, or where your new documentation completely substantiates all your original positions. If this happens, any payments you've made toward the disputed assessment will be refunded with interest.Partial Adjustment is probably the most common outcome. The IRS agrees with some of your points but not others, or they agree that an adjustment is warranted but not to the extent you requested. For instance, you might have claimed $10,000 in business expenses that were disallowed, and the IRS might accept $6,000 based on your documentation. While this might be disappointing if you were hoping for full vindication, it's still a positive outcome that reduces your tax burden.IRS Stands by Original Audit Findings is obviously the outcome you don't want, but it happens more often than you might think. Sometimes the new documentation isn't as compelling as you thought, or the IRS error you believed existed was actually correct application of the law. If this happens, you'll receive a letter explaining why your request was denied. The letter should address each point you raised and explain why the IRS maintains its position.Regardless of the outcome, the IRS should provide a clear explanation of their determination.If they've made adjustments, they'll include revised calculations showing how they arrived at the new figures.If they've denied your request, they should explain why your arguments or documentation weren't sufficient.

Why Legal Help Matters

The harsh reality about IRS collection actions is that the system isn't designed to be fair—it's designed to be efficient at collecting revenue. The IRS has virtually unlimited resources, decades of institutional knowledge, and collection powers that would make any other creditor envious. You, on the other hand, are likely dealing with tax law for the first time while simultaneously managing the stress of potential financial ruin. It's not a fair fight, and going it alone is like representing yourself in court against a team of experienced prosecutors.

Your Tax Crisis Doesn't Have to Define Your Future

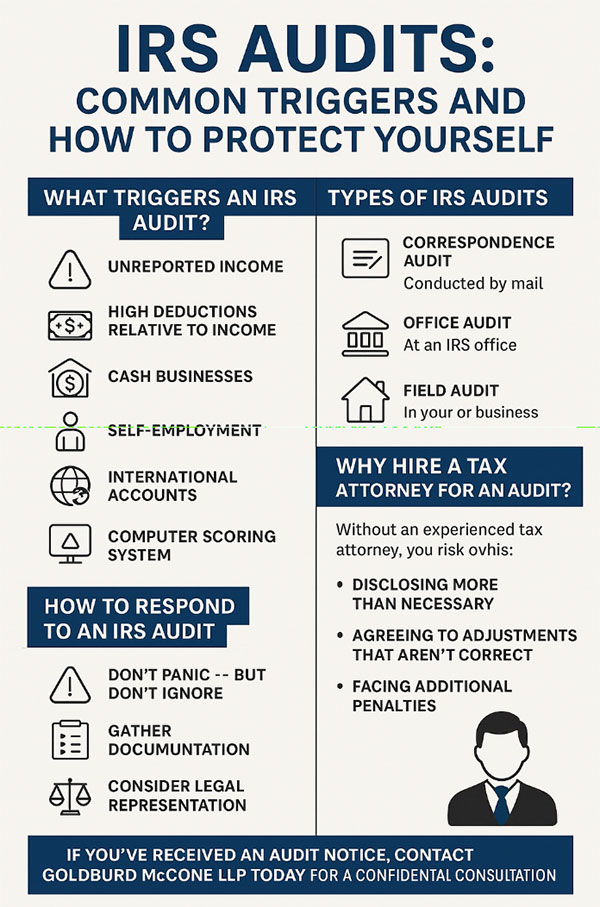

IRS collection actions can feel like a financial death sentence, but they don't have to be. Whether you're facing a wage levy that's destroying your ability to pay bills, a lien that's blocking a crucial refinancing, or an overwhelming tax debt that seems impossible to escape, there's almost always a path forward—if you know where to look and how to navigate it.Don't let another day pass watching your tax problem grow worse. Contact Goldburd McCone today.]]>On Behalf of Goldburd McCone LLP<![CDATA[What Triggers an IRS Audit?]]>https://www.goldburdmccone.com/?p=2606482026-01-07T21:01:18Z2026-01-07T20:55:06Zwhat triggers an IRS audit and how to respond effectively can put you back in control.

At Goldburd McCone LLP, we defend individuals and businesses facing audits every day — ensuring the IRS stays within its bounds and taxpayers’ rights are protected.

What Triggers an IRS Audit?

IRS audits aren’t random. While the IRS does conduct some random examinations, most audits are triggered by specific factors.

Unreported Income

You know all those forms you get in the mail each year—W-2s from your employer, 1099s from your bank, maybe a few from freelance clients?

Well, the IRS gets copies of every single one of these too.

When something doesn't match up, even by a small amount, their system immediately takes notice.

It's surprisingly easy to accidentally leave something off your return. Maybe you switched banks mid-year and forgot about that small interest payment from your old savings account. Or perhaps you did a one-off consulting gig and the 1099 got lost in your email.

Sometimes people genuinely forget about unemployment compensation they received early in the year.

Even a tiny discrepancy, say $50 in unreported interest, can trigger an inquiry.

That's why keeping a folder (physical or digital) for all your tax documents throughout the year is so valuable. When tax time rolls around, you can cross-check everything against your records rather than relying on memory.

High Deductions Relative to Income

When your deductions are way outside the norms of your income, their systems take notice.

Now, this doesn't mean you should be afraid to claim every legitimate deduction you're entitled to—that's your right as a taxpayer.

But if you donated half your income to charity last year, or if your home office deduction seems large relative to your income, you'll want to make sure you've got rock-solid documentation.

We're talking receipts, cancelled checks, acknowledgement letters from charities, etc.

The truth is, unusual situations do happen. Maybe you had extensive medical expenses due to an unexpected illness, or you made an exceptionally generous charitable contribution after selling some investments.

The IRS understands that real life doesn't always fit neatly into statistical averages. But they'll want to verify that these outlier deductions are real, so having your paperwork in order from the start saves everyone time and stress.

Cash Businesses

If you run a restaurant, hair salon, food truck, or any business where cash changes hands regularly, you're probably already aware that the IRS pays closer attention to your industry.

It's not that they think everyone in these businesses is dishonest—they just know from experience that cash creates opportunities for income to slip through the cracks, whether intentionally or through simple bookkeeping oversights.

Think about it from their perspective: when someone pays with a credit card, there's an electronic trail. When they pay cash, the only record might be a handwritten receipt or a number jotted in a notebook.

That's why businesses that deal heavily in cash need to be extra diligent about their record-keeping.

If this is you, consider making your life easier (and audit-proof) by depositing cash receipts regularly and keeping them intact—resist the temptation to take out your salary or pay expenses directly from the till.

Keep detailed daily records, maybe invest in a point-of-sale system that tracks everything automatically, and for heaven's sake, keep your business and personal finances separate.

Yes, it's more work, but it's far less work than dealing with an audit. Plus, good records actually help you understand your business better, so it's a win-win.

Self-Employment

Being self-employed comes with amazing freedom, but it also comes with increased IRS scrutiny.

Schedule C filers face audit rates several times higher than regular wage earners, and while that might seem unfair, there's a certain logic to it.

When you're self-employed, you have more control over how you report income and expenses, and the rules are genuinely more complex.

The IRS has seen it all when it comes to questionable Schedule C deductions—the person who claims their entire car payment as a business expense despite only using it for business 20% of the time, or the "consulting business" that reports losses year after year while the owner maintains a suspiciously comfortable lifestyle.

These patterns have made them skeptical, which means legitimate self-employed folks need to be extra careful.

If you're self-employed, treat your business like a business, even if you're working from your kitchen table.

Get a separate bank account and credit card for business expenses (this makes tax time so much easier anyway).

Keep a mileage log that would make your most detail-oriented friend proud. Save every receipt, and write notes on them about the business purpose if it's not obvious.

And if your business has been losing money for several years, be prepared to show that you're genuinely trying to make a profit—otherwise, the IRS might reclassify your business as a hobby, and there goes your ability to deduct those losses.

International Accounts

If you have money in foreign banks or investments overseas, you're dealing with some of the most complex areas of tax law.

The IRS has really cracked down on international tax compliance over the past decade, and the penalties for getting it wrong can be absolutely crushing—we're talking penalties that can exceed the value of the accounts themselves.

The tricky part is that the rules are genuinely confusing.

Many people don't realize that their foreign mutual fund requires special reporting, or that the foreign bank account they inherited from their grandmother needs to be disclosed even if they never touch the money.

And if your foreign accounts total more than $10,000 at any point during the year, you need to file an FBAR. Miss that deadline, and you could face serious consequences.

If you have any international financial connections—whether it's a bank account from when you worked abroad, foreign investments, or rental property in another country—don't try to navigate this alone.

Find a tax professional who actually understands international taxation.

Computer Scoring System

The Discriminant Inventory Function (DIF) sounds like something out of a spy novel, but it's actually the computer scoring system the IRS uses to decide which returns deserve a closer look.

Think of it as an incredibly sophisticated program that looks at hundreds of different factors on your return and compares them to millions of other returns to spot anything unusual.

Nobody outside the IRS knows exactly how the DIF formula works, it's one of their most closely guarded secrets.

But we do know it looks at relationships between different numbers on your return. For instance, if you're reporting a modest income but claiming mortgage interest on a million-dollar home, that's going to raise questions. Or if your business expenses are completely out of line with others in your industry, the system will flag it.

The important thing to remember is that having a high DIF score doesn't mean you've done anything wrong. Plenty of people have legitimate reasons for being statistical outliers.

Maybe you had an unusual financial event this year, or your situation is genuinely different from the norm. That's fine—just make sure you can back up everything on your return with solid documentation. The IRS knows that real life is messy and complicated. They just want to make sure that when someone's return looks unusual, there's a real story behind it, not creative accounting.Types of IRS Audits

Correspondence Audit – Conducted by mail; usually limited to specific issues.

Office Audit – You are asked to appear at an IRS office with documents.

Field Audit – IRS agents come to your home or business; the most intrusive type.

How to Respond to an IRS Audit

Don’t panic — but don’t ignore. Respond promptly to deadlines.

Gather documentation. Receipts, bank statements, invoices, contracts.

Limit communication. Don’t overshare; only provide what is requested.

Consider legal representation. A tax attorney ensures compliance while protecting you from unnecessary exposure.

Appeal if necessary. If you disagree with audit findings, you have rights to reconsideration and appeals.

Why Hire a Tax Attorney for an Audit?The IRS has skilled examiners whose job is to maximize tax collection. Without experienced representation, you risk:

Disclosing more than necessary.

Agreeing to adjustments that aren’t correct.

Facing additional penalties.

Goldburd McCone LLP represents clients in New York, New Jersey, and nationwide to resolve audits efficiently and favorably.Conclusion & CTAAn IRS audit doesn’t have to derail your finances. With the right strategy, you can respond effectively and protect your rights.If you’ve received an audit notice, contact Goldburd McCone LLP today for a confidential consultation.]]>On Behalf of Goldburd McCone LLP<![CDATA[Tax fraud revelation: Lessons from the Magician’s case]]>https://www.goldburdmccone.com/?p=2606072025-12-19T08:32:10Z2026-01-01T08:31:34ZHow was the fraud uncovered?

Alvarez is the CEO of ATAX New York, a Bronx-based high‑volume tax prep company. From 2010 to 2020, he and his employees filed tens of thousands of fraudulent individual tax returns. His team inserted fake deductions, invented business losses and claimed phony tax credits to inflate refunds and reduce liabilities for their clients.

Alvarez purposely hired and trained people to work with false data. Some employees claimed they were aggressively intimidated when they questioned him. Eventually, the IRS uncovered $145 million in lost tax revenue and over $11 million in fraudulent proceeds all gained by Alvarez. It was an extensive operation that involved a huge amount of time and resources spent reviewing returns, talking to witnesses as well as tracing manipulated financial records.

What taxpayers need to learn from the Magician

Your tax preparer’s license should not be your only consideration when hiring. Here are some warning signs that suggest the company may not be compliant:

You get unusually large refunds that are inconsistent with your income.

You were advised to fabricate deductions or credits under the guise of good faith.

Delaying delivery of copies of your return or documentation.

High-pressure tactics to sign blank or incomplete forms.

If you ever recognize any of these issues, report it to the IRS right away. You can also file a complaint with the New York State attorney general and the New York State Department of Taxation and Finance. If you want to stop the preparer from harming other clients, report them to the appropriate professional board or local law enforcement for criminal activity.

Penalties and consequences

Alvarez currently faces potential penalties that include up to five years for conspiracy and three years for aiding false returns, along with restitution and forfeiture of illicit gains.

Avoid dishonest preparers

To avoid liability, vet your tax preparer and maintain your own records so you can use them as a comparison. Be vigilant and keep clear documentation to protect yourself in case of audits or disputes. If you are accused of tax fraud because of your preparer’s negligence or willful acts, a tax fraud attorney can defend you and fight for your rights.]]>On Behalf of Goldburd McCone LLP<![CDATA[Tips to help manage tax debt]]>https://www.goldburdmccone.com/?p=2604582025-11-19T21:50:43Z2025-11-26T21:45:41Z Internal Revenue Service (IRS) is notoriously aggressive when it comes to collecting on debt. They have many different legal tools they can use to help gather what is owed, from taking money right out of your paycheck to seizing your assets. Taxpayers who find themselves in this situation have options. The following will discuss common mistakes people make when trying to manage their tax debt and provide three alternatives that are more likely to set you up for future financial success.

Avoid these common mistakes

It is important to avoid making mistakes that only complicate the situation. Common examples include:

Ignoring the issue. One of the biggest mistakes is not taking growing tax debt seriously. There are options to help get control over the situation.

Failing to file a return. The IRS has more tools now than ever before. It is extremely unlikely that you can simply fly under the radar. The agency will notice if you are not filing tax returns.

Choosing the wrong debt management option. It is important to review the pros and cons of each and tailor a plan to your specific situation.

Whether one of the mistakes noted above led to your current debt or you found yourself facing unmanageable tax debt for a different reason, there are options that can help you address the situation. One of the most common is an installment agreement (IA). This option is essentially a payment plan between the taxpayer and the IRS. Taxpayers can choose a short or long-term repayment plan depending on their situation. Another option is an offer in compromise. As the name suggests, this option involves a compromise between the IRS and the taxpayer. In certain situations, taxpayers who are unable to pay the outstanding tax balance can convince the IRS to accept a lesser amount. Taxpayers can tailor one of these debt management options to best suit their needs. Determining the best course of action will depend on the details of your situation. As such, it is wise to seek legal counsel from those with experience in this area of law. The attorneys at Goldburd McCone can discuss these and other options to help you regain control of your finances when dealing with the IRS.]]>On Behalf of Goldburd McCone LLP<![CDATA[How do I prepare for a residency audit?]]>https://www.goldburdmccone.com/?p=2595902026-01-21T14:32:23Z2025-10-06T17:50:12Zhighly motivated to establish that any attempt to leave the state is an effort to avoid tax obligations. If successful, you could still find yourself owing New York state taxes.

This aggressive enforcement posture has led to an increase in residency audits. Understanding how aggressively New York conducts residency audits helps explain why preparation is critical.

As a result, anyone considering a move to another state—or who has recently made the move—should take steps to ensure they have the evidence needed to refute claims from state taxing authorities. Three important tips include the following:

Time matters

Where you spend your time matters. It is very helpful if you can clearly show that you spent most of your days in your intended home state. Keep a journal of where you spend your time and maintain documents to back it up. This could include receipts from restaurants, hairdressers, and auto mechanics. Tracking days carefully is especially important given New York’s strict day-count rules, which are frequently examined during residency audits, including those discussed in audits involving snowbirds and frequent travelers.

Move your things

Your car, your art, your jewelry, even your pets. Make sure you move the items you use in daily life as well as those with sentimental value to your new home state. State auditors often focus on where a taxpayer’s most “near and dear” possessions are located when determining domicile.

Go public

Do not underestimate the power of social media. Let others know that you now consider Florida—or whichever state you move to—your home. While social media alone is not decisive, it can serve as supporting evidence when combined with stronger documentation.

These are just a few of many steps that can help you build evidence to verify your move. Once you have taken these steps, it is important to organize your records carefully. Keep journals, receipts, and supporting documents readily available. If you receive a notice from the state, understanding how tax audits typically proceed can help reduce uncertainty and stress.

If you receive notification of an official residency audit, you do not have to face it alone. You have the right to legal counsel. The attorneys at Goldburd McCone have experience in this complex area of tax law and can advocate for your interests, helping ensure your rights are protected throughout the audit process.]]>